Cheat On Your Diet, Not Your Retirement Plan

Sept 14, 2020 | Lena Rizkallah, JD, CRPC®

It seems that everyone is on some type of diet these days. Whether it’s no carb/high protein; high protein/high fat/low sugar; no sugar/no carb/no fat/no dairy/all bacon—it seems like everyone has an eating plan. My neighbor is on the starvation diet, my good friend is KETO-ing, another friend hasn’t had a slice of bread in 3 years, and my sister and her husband have decided to ‘eat clean,’ whatever that is. Despite all the random rules and vast differences between all of these diets, most plans allow for an occasional “cheat day.” That’s the day that you can eat whatever the heck you want.

As someone who never skips a meal, never says no to a fresh baguette and cheese, and believes that life is short, all of that sounds like a nightmare to me. Basically, for me, every day is a cheat day.

These strict diet plans are philosophically similar to planning for income in retirement. Once you stop working and are relying on your retirement portfolio and Social Security for income for the rest of your life, it’s important to establish a withdrawal strategy that will provide you the consistent income you need to maintain your lifestyle—and to stick to the plan. A disciplined approach to managing your money in retirement, along with a few cheat days along the way, could help make sure that you fulfill all the goals you have for yourself in retirement without outliving your money.

When building a retirement income plan and deciding on a withdrawal strategy, you should think about the following variables:

- How long you and/or your spouse could live. Remember that life expectancy is increasing. The average 65-year-old couple today has almost a 50% chance that one of them will live to at least age 90 (SSA.gov).

- How much do you need for necessities? Do you plan to retire and stay in your home or will you move to a lower tax state and downsize? Note that housing costs continue to take the biggest bite out of your budget even in retirement; that includes not only mortgage or rent but also utilities, property tax, cable and upkeep.

- Do you expect to spend a lot on health care expenses? Many people will enter retirement relatively healthy and later in their late ‘70’s or ‘80’s may experience a long-term care (LTC) event. Others may already have a history of health problems early on, so it’s important to consider health care in your financial plan and budget for it. Remember that health care is the fastest growing cost in retirement, so your starting costs at age 65 could increase significantly ten or more years later.

- What’s on your bucket list? Beyond the necessities, what else do you expect to spend money on in retirement? Consider travel, hobbies, and how you intend to spend your free time as potential budget items when discussing plans with your advisor.

- What is your risk tolerance? Most people enter retirement with a very conservative mindset; they figure that their nest egg should last them another 25 or more years, and therefore have low tolerance for participation in the equity markets or alternative investments. While this may seem “safe” the risk is missing out on the returns necessary for longer life expectancy, rising health care costs and an overflowing bucket list.

There are many ways to manage all the sources of your retirement income to come up with the right withdrawal strategy. Here are three of the main strategies:

- The 4% Rule. For many years, this was the “rule of thumb” that many advisors used for pulling money out of a retirement portfolio. The rule provides that upon retirement, you would withdraw an initial 4% from your retirement portfolio. For a $1 million portfolio, you can withdraw $40,000 the first year of retirement. Thereafter, you would adjust that initial withdrawal amount by inflation (generally 2%) every year to keep up with the cost of living. The theory goes that in utilizing this strategy, there is a high likelihood that you would never outlive your retirement portfolio. However, critics have chimed in about the shortcomings of the research including variances in market conditions over time as well as the probability of having too much money unintentionally left over.

- The bucket strategy. With this strategy, you would arrange and invest your portfolio according to your near-term, intermediate, and long-term needs. Your near-term needs—think emergency fund, day-to-day, housing costs and other costs that would need to be funded in the next 3-5 years—would be invested in cash so that this bucket is accessible and liquid at all times. The intermediate bucket is invested for a 5-10 year time frame; this bucket includes cash as well as bonds and some equities since the longer time frame allows for a potential for long-term returns. The long-term bucket has the longest investing timeframe- 10-20+ years and thus could hold a long-term diversified portfolio that includes equities and alternative investments. As the near-term bucket is used, certain positions in the intermediate and long-term buckets are shifted, sold off or rebalanced in order to replenish the needed funds.

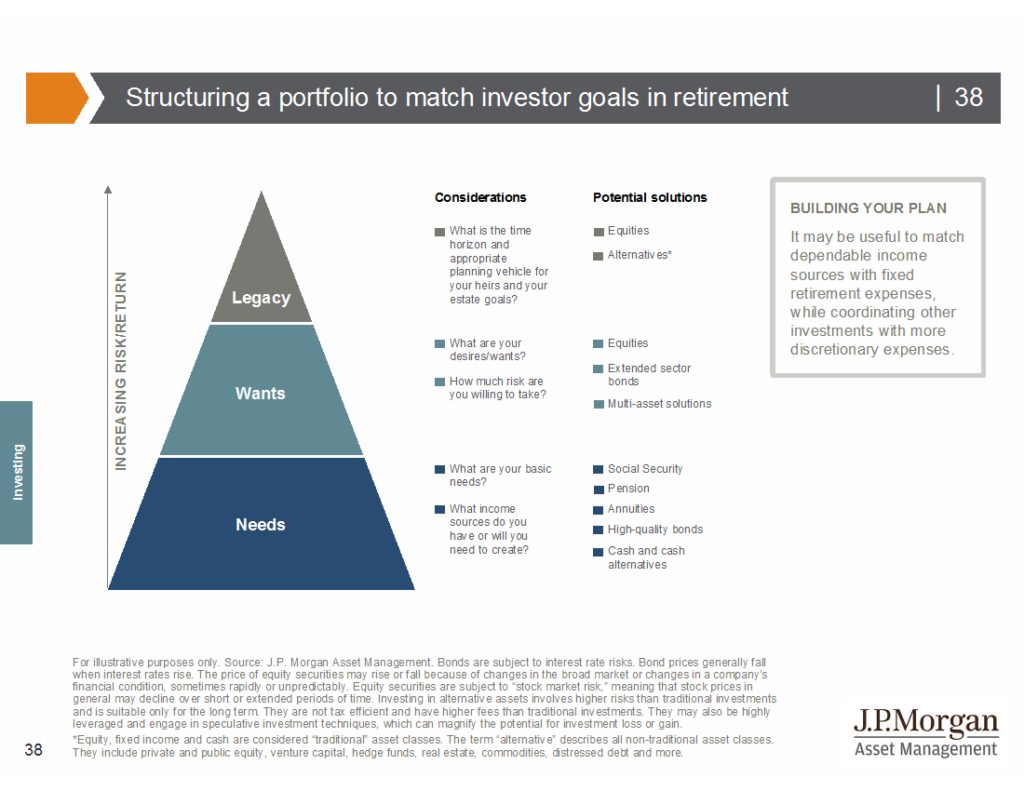

- Guarantee the floor strategy. With this strategy, think of your goals as a pyramid illustrated in the JP Morgan slide below. At the bottom of the pyramid are your ‘needs.’ This rung is funded with all of your ‘guaranteed,’ non-risky sources of income that are not subject to market conditions, like cash, Social Security benefits, pension and annuity payments. The middle portion is your ‘wants,’ which include vacations, hobbies, and the ability to elevate your lifestyle and have some financial freedom in retirement. This portion is invested in a diversified portfolio that includes bonds and some equities to help grow your money. The top part of the triangle is your ‘legacy,’ and this is the amount of your portfolio that you want to leave to children, organizations, and other beneficiaries. Since this is the portion of your portfolio that you don’t necessarily intend to use, you may invest these funds in riskier asset classes like alternative investments to produce potentially higher returns.

Deciding on the right withdrawal strategy, like a diet plan, is a very personal decision; it takes discipline, structure and an understanding that putting the right strategy in place and following it through could help you potentially reach your goals. Splurging on a beach vacation or fancy dinner out, like eating cheesecake on a cheat day, is totally OK as long as you are following the long-term plan.